Our financial system is crumbling this week.

-

AWvsCBsteeeerike3

- "I could totally eat a pig butt, if smoked correctly!"

- Posts: 27537

- Joined: August 5 08, 11:24 am

- Location: Thinking of the Children

Re: Our financial system is crumbling this week.

also, not for retirement but for family, whole life insurance policies are worth looking into.

-

Michael

- GRB Founder

- Posts: 35303

- Joined: December 31 69, 6:00 pm

- Location: Chicago, IL

- Contact:

Re: Our financial system is crumbling this week.

I agree, that is why the 3 fund portfolio, which is my investment strategy, includes bonds. I also own real estate (my home). With that combination I'm extremely diversified.AWvsCBsteeeerike3 wrote:I find it hard to believe that someone can be truly diversified in the stock market alone.

I agree, that's why I do the 3 fund portfolio, which includes bonds and international.AWvsCBsteeeerike3 wrote:Total market funds may provide protection against secular downturns but they're still reliant on the general health of America.

AWvsCBsteeeerike3 wrote:So if you want my advice it would be to figure out how much is needed for retirement. Assume you get like 25% from ss and whatever else.

Take the average age of death and use that.

Calculate how much you need for retirement based on your current paycheck. Account for inflation and calf how much you'll spend bw 62 ish and 78ish.

Personally, I use this retirement calculator that runs various simulations to determine how I'm doing. It's not perfect, but it is helpful.

I strongly disagree with path 3. Study after study shows even "experts" are really bad at speculation. You might as well throw darts at a board with investment vehicles. Also, by buying individual stocks you're introducing significant portfolio risk.AWvsCBsteeeerike3 wrote:Then provide 3 different ways to get there.

Path 1. Iras, 401ks; etc.

Path2. Housing. In other words find somewhere somehow to buy the home you pay for and enjoy the small benefits.

Path 3. Self controlled investments. Invest in silver, Tessa, amazon, Facebook or klondex. I would argue it doesn't matter who so long as you know them well. Use your own after tax money.

Jack Bogle said "Simplicity is the master key to financial success."

I agree. The low cost 3 fund portfolio with tax-efficient fund placement is easy to do and leverages modern portfolio theory. It's also lower stress way to invest.

I agree. Many retirement instruments insurance companies sell, like annuities, are really bad.AWvsCBsteeeerike3 wrote:also, not for retirement but for family, whole life insurance policies are worth looking into.

-

AWvsCBsteeeerike3

- "I could totally eat a pig butt, if smoked correctly!"

- Posts: 27537

- Joined: August 5 08, 11:24 am

- Location: Thinking of the Children

Re: Our financial system is crumbling this week.

I think where we probably disagree the most is on how connected the global economy is.

Take 2009 for example. Home values took a dump. And, so did every stock market in the world. Bonds didn't suffer, relatively, but they also took a bit of a hit.

Even the most diversified portfolio isn't going to be protected from downturns like 2009. Now, it's impossible to protect, in a portfolio, against armageddon, right? I think we agree on that as well.

But, with enough liquidity and, well, ability, it's entirely possible to hedge against the downturns with the liquidity. Take 2008 for example. As the stock market was soaring, gold was crashing. Then, the two completely flip flopped. Gold soared as the stock market tanked. Of course, there's risk associated with buying gold as a long term investment. But, it was an incredibly wise trade in hindsight to purchase it as everyone looked for a safe place to store money.

Will that happen again in our lifetimes? I don't know. I tend to doubt it and hope it doesn't. But, when broad markets fail, people still want their money to work. Where they go with it will have an inherent increase in value.

Take 2009 for example. Home values took a dump. And, so did every stock market in the world. Bonds didn't suffer, relatively, but they also took a bit of a hit.

Even the most diversified portfolio isn't going to be protected from downturns like 2009. Now, it's impossible to protect, in a portfolio, against armageddon, right? I think we agree on that as well.

But, with enough liquidity and, well, ability, it's entirely possible to hedge against the downturns with the liquidity. Take 2008 for example. As the stock market was soaring, gold was crashing. Then, the two completely flip flopped. Gold soared as the stock market tanked. Of course, there's risk associated with buying gold as a long term investment. But, it was an incredibly wise trade in hindsight to purchase it as everyone looked for a safe place to store money.

Will that happen again in our lifetimes? I don't know. I tend to doubt it and hope it doesn't. But, when broad markets fail, people still want their money to work. Where they go with it will have an inherent increase in value.

-

sighyoung

- Mayor of GRB

- Posts: 38544

- Joined: April 17 06, 7:42 pm

- Location: Louisville

Re: Our financial system is crumbling this week.

I've just been dipping my toe in this thread, so forgive me if my question has already been covered. But do those write-ups on 3-fund-portfolio investing discuss shifting percentages as one ages? I'm now in my mid-fifties, and am invested in Fidelity Freedom 2030 funds for my 403(b). Reducing fund expenses by close to .75% is very attractive, but obviously I'd need to shift around assets myself as I get older.

-

Michael

- GRB Founder

- Posts: 35303

- Joined: December 31 69, 6:00 pm

- Location: Chicago, IL

- Contact:

Re: Our financial system is crumbling this week.

I think you're advocating timing the market via "liquidity" based on what you think will happen. I fundamentally disagree with that approach. My 3 fund portfolio is a reasonable yet risk diversified adverse approach to investing, and depending on where you put your money and situation offers liquidity . Loading up on gold doesn't really offer that. I'm not saying the 3 fund portfolio is for everyone (although I think it's what most people should be doing), but it works amazingly well.AWvsCBsteeeerike3 wrote:I think where we probably disagree the most is on how connected the global economy is.

Take 2009 for example. Home values took a dump. And, so did every stock market in the world. Bonds didn't suffer, relatively, but they also took a bit of a hit.

Even the most diversified portfolio isn't going to be protected from downturns like 2009. Now, it's impossible to protect, in a portfolio, against armageddon, right? I think we agree on that as well.

But, with enough liquidity and, well, ability, it's entirely possible to hedge against the downturns with the liquidity. Take 2008 for example. As the stock market was soaring, gold was crashing. Then, the two completely flip flopped. Gold soared as the stock market tanked. Of course, there's risk associated with buying gold as a long term investment. But, it was an incredibly wise trade in hindsight to purchase it as everyone looked for a safe place to store money.

Will that happen again in our lifetimes? I don't know. I tend to doubt it and hope it doesn't. But, when broad markets fail, people still want their money to work. Where they go with it will have an inherent increase in value.

This is a great question that has no perfect answer. It ultimately comes down to your willingness to handle risk. How have you dealt with downswings in the past? If the stock market drops 25% will you sell due to your concerns? If so, you'll want a higher % of bonds because they are a more conservative investment than equities.sighyoung wrote:I've just been dipping my toe in this thread, so forgive me if my question has already been covered. But do those write-ups on 3-fund-portfolio investing discuss shifting percentages as one ages? I'm now in my mid-fifties, and am invested in Fidelity Freedom 2030 funds for my 403(b). Reducing fund expenses by close to .75% is very attractive, but obviously I'd need to shift around assets myself as I get older.

A good place to start looking for allocations is the vanguard target date retirement funds. For example, if you project your retirement to be 2030ish Vanguard has the following asset allocation:

72% Equities

28% Bonds

60% Domestic Equities

40% International Equities

Here's the Fidelity Freedom 2030:

82.5% Equities

16.5% Bonds

1% Other

66% Domestic Equities

34% International Equities

As you grow older you can check back in with these funds and adjust accordingly. You should expect the % of bonds to increase as you age.

I'm actually a bit surprised how aggressive the Fidelity fund is with the equities to bond ratio. I'm not saying they are wrong, but I just would have expected something a bit closer to Vanguard. Some advisers recommend investors should take 100 minus your age to determine your equities allocation. For example, if you're 55, you'd be 45 equities and 55 bonds. Personally, I think that's too conservative, but everyone is different.

I'm 40 and here's my current allocation:

84% Equities

16% Bonds

77% Domestic Equities

23% international Equities

I'm currently boosting my international %. I'd like international to be closer to 30%. That said, a Vanguard white paper suggests at least 20% of international equities provides around 80% of volatility diversification benefits of full world market weighting (45% vs 55%). Therefore, at a minimum I'd do 20% international of the equities allocation pie. On the flip side, Warren Buffet recommends no international stocks, which is outside mainstream financial portfolio theory.

Finally, make sure you're tax efficient and re-balance your %s once a year. Also, don't try and time the market with your allocations based on your "gut feeling" or some article you read on cnbc. It wouldn't hurt to have an allocation plan now as you age and stick with it. After you decide your course make peace with your yourself and realize nothing is guaranteed. You can only make the best decisions possible with the information you have.

*Michael LLC is not a licensed financial adviser and provides investment advice for entertainment purposes only. Not available in all 50 states. Void where prohibited.

edit - here's an asset allocation article: https://www.bogleheads.org/wiki/Asset_allocation

Last edited by Michael on July 25 17, 2:48 pm, edited 1 time in total.

-

Michael

- GRB Founder

- Posts: 35303

- Joined: December 31 69, 6:00 pm

- Location: Chicago, IL

- Contact:

Re: Our financial system is crumbling this week.

An article that mentions the 3 fund portfolio study:

The results for active index funds are even worse when you factor survivor bias.

LinkIn 2013, Rick Ferri, CFA and Alex Benke, CFP® released the results of a study where they compared the performance of actively managed investment portfolios to those of index-based portfolios.

The actively managed approach relies on the skill and expertise of investment professionals to generate superior returns. The index-based approach relies on mutual funds and ETFs that simply track the market.

What they found was pretty incredible.

Despite all of their training, all of their knowledge, and all of the time spent trying to find the best opportunities, the investment professionals repeatedly failed to beat a simple index-based investment strategy.

For example, when Ferri and Benke evaluated a simple three fund portfolio made up of US stocks, international stocks, and US bonds, they found that the index-based portfolio outperformed the actively managed portfolio 82.9% of the time.

Not only that, but the professionals typically underperformed by 1.25% per year. And the small number of professionals who managed to outperform the market only did so by 0.52% per year.

In other words, not only were there far fewer winners than losers, but the losers lost by much more than the winners won by.

Now, you could argue that a three fund portfolio is too simple and therefore not a fair comparison. After all, most investment professionals create more complicated portfolios in an effort to capture extra returns and limit the downside risk.

Luckily, Ferri and Benke looked at that scenario too.

What they found was that the more complicated you made the portfolio, the more likely it was that the index-based strategy would win. For example, when they looked at a 10-fund portfolio that included a wide range of asset classes, the index-based portfolio produced better returns 89.9% of the time.

And by the way, these were not isolated findings. Study after study has demonstrated the superiority of index funds over actively managed funds.

The big breakthrough here was the realization that combining index funds in a portfolio increases that advantage even further.

That finding has some pretty powerful implications for you as you create your own personal investment plan.

The results for active index funds are even worse when you factor survivor bias.

-

Arthur Dent

- Hall Of Famer

- Posts: 12527

- Joined: April 25 06, 6:43 pm

- Location: Austin

Re: Our financial system is crumbling this week.

Regardless of what asset allocation between bonds/stocks and domestic/international is optimal, Fidelity's 0.7% expense ratio seems excessive. Switching to Vanguard's target date fund saves you 0.55% a year, though employer plans may not have it available. My 401k allows me to pay a small annual flat fee, to use an online brokerage where you can invest in all the usual stuff, which I have done. Dunno how common that is.

Fidelity also strikes me as excessively risky for retirement for in ~15 years (though what's actually optimal is fuzzy, and I have no real insight personally), but if you wanted that allocation, you could still save on expenses by recreating it with a mix of equivalent lower expense funds.

Fidelity also strikes me as excessively risky for retirement for in ~15 years (though what's actually optimal is fuzzy, and I have no real insight personally), but if you wanted that allocation, you could still save on expenses by recreating it with a mix of equivalent lower expense funds.

-

Michael

- GRB Founder

- Posts: 35303

- Joined: December 31 69, 6:00 pm

- Location: Chicago, IL

- Contact:

Re: Our financial system is crumbling this week.

If my employer offered Vanguard's target date fund I'd just do that for ease. Instead I have Fidelity and their high target date fees. Fortunately, I have access to low cost funds to create the 3 fund portfolio. One caveat - my Fidelity 401k doesn't offer a domestic total market fund, so I use an S&P 500 fund instead. All things being equal I'd rather have a US total market fund, but the historical performance differences are minor.

That brokerage option is really nice, AD. I'm jelly.

That brokerage option is really nice, AD. I'm jelly.

-

Michael

- GRB Founder

- Posts: 35303

- Joined: December 31 69, 6:00 pm

- Location: Chicago, IL

- Contact:

Re: Our financial system is crumbling this week.

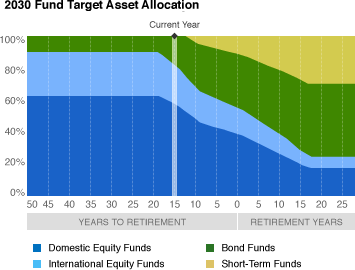

Looking closer at that 2030 Fidelity fund, and its equities vs bond ratio, it appears the fund is hitting an inflection point where it's about to really ramp up the bond allocation:

This fund also adds short-term funds which are low risk. Vanguard doesn't bother with those until retirement.

Eyeballing the chart, it also appears sometimes the fund's domestic to international ratio tilts toward domestic as it ages, which I don't completely understand. With Vanguard's target fund the domestic to international ratio is static, while equities to bond ratio adjusts over time, which makes sense to me. Maybe my eyes are playing tricks on me.

This fund also adds short-term funds which are low risk. Vanguard doesn't bother with those until retirement.

Eyeballing the chart, it also appears sometimes the fund's domestic to international ratio tilts toward domestic as it ages, which I don't completely understand. With Vanguard's target fund the domestic to international ratio is static, while equities to bond ratio adjusts over time, which makes sense to me. Maybe my eyes are playing tricks on me.

-

Arthur Dent

- Hall Of Famer

- Posts: 12527

- Joined: April 25 06, 6:43 pm

- Location: Austin

Re: Our financial system is crumbling this week.

Don't international investments, on average, carry more risk for the at equivalent returns because of currency risk? Diversification from the non-correlation to the U.S. will still improve portfolio risk-adjusted returns, but because of the added risk, couldn't you bring down portfolio risk with age on the foreign/domestic axis as well is the bonds/equities one? Have not looked into whether it makes sense to proceed on just one or both of those.Michael wrote:Eyeballing the chart, it also appears sometimes the fund's domestic to international ratio tilts toward domestic as it ages, which I don't completely understand. With Vanguard's target fund the domestic to international ratio is static, while equities to bond ratio adjusts over time, which makes sense to me. Maybe my eyes are playing tricks on me.

Somewhat relatedly, do you know anything about Vanguard's international bond allocation in their target funds? Seems like international bonds would be a worse deal than international stocks as the exact same currency risk gets added on but at a lower average return.